The U.S. investment situation is rooted in daily life unlike Japan

As the aging society progresses, the challenge of asset building for retirement is becoming more and more important. However, while household financial assets have increased as much as 2.3 times in the U.K. and 3.4 times in the U.S. within about 20 years since 2000, they have only increased 1.4 times in Japan. In Europe and the U.S., as it is difficult to increase assets only by earned income, they invest at the same time and increase their income in tandem. As people are focused on earned income in Japan, their stability is like that of a unicycle.

Pension and health insurance are heavy burdens for Japan’s spending. As the aging society progresses, it is obvious that these costs will increase. If we work hard, we do not need to think about asset building for retirement. This was the case in the past. Today, we cannot continue to be completely dependent on our country and companies. In the U.S. since the 1980s, people have been encouraged to make self-directed efforts because the public pension is not sustainable anymore. Even those in the U.S. are trying to support themselves with the 3-legged stool of public pension, company pension, and their own savings and investments. On the other hand, Japan, of which the population aging rate is the highest in the world, has only 2 legs with limited self-directed efforts. This is worrisome. Although the situation is already dire, the sense of crisis is not well shared.

When personal financial assets are compared, in the U.S., cash and deposits only account for a little more than 10% and others consist of investment products and insurance and pension, etc. In Japan, however, cash and deposits account for 50% or more. If the interest rate of 0.001% for ordinary deposits continues, it will take 72,000 years to double the principal. If the yield is 3%, it will take 24 years to achieve that goal, and if it is 6%, it will take 12 years. You can duly double the amount during your working years. For investment purposes, this figure may be feasible.

Investment is rooted in Americans because the idea of financial well-being (FWB), which shows that a healthy financial state is prevalent. The Consumer Financial Protection Bureau, which was established in response to the 2008 financial crisis, defined FWB, after conducting a major investigation. You “have control over day-to-day, month-to-month finances,” “have the capacity to absorb a financial shock,” “have the financial freedom to make the choices that allow you to enjoy life,” and “are on track to meet your financial goals.” The U.S. thinks that these four are the factors of FWB.

Americans will invest because they understand their own ideal FWB and try to achieve or maintain it. Americans share the common recognition that having a low salary or not being rich should not prevent them from pursuing their own FWB. Moreover, the recognition that financial shocks are unavoidable has spread. Their awareness has been changed from zero-risk to with-risk, just like changing from zero-Covid to with-Covid. Therefore, let’s be prepared to alleviate the pain as much as possible, instead of stopping investing to avoid the pain. Such awareness seems to be rooted in American people.

Customer-oriented business conduct to move toward a healthy financial state

If we compare it to the human body, the optimal weight depends on their height or exercise level. However, there is a broad consensus that “excessive weight is not good.” Such broad consensus corresponds to FWB in finance, but this is not defined in Japan. On the contrary, the negative sales custom of recommending affiliated or high-commission products or churning at the expense of customers’ interests has made investment difficult. Churning means excessive trading to maximize commissions whether or not the investment is going well. If they keep doing this, it is natural that customers will not trust sales representatives.

In response, in 2017, the Financial Services Agency published the “Principles for Customer-Oriented Business Conduct (similar to the US Best Interest Rule).” They first tried to eliminate issues such as churning, but they also aimed for the prevalence of actual customer-oriented conduct. Investment is wide-spread in Europe and the U.S. because various services are provided to various types of customers with different needs. Even if the return is high, oversophisticated products are inappropriate for risk-adverse low-asset individuals, and if someone who is not rich or someone who does not like investing is recommended to invest in advanced and complicated products, there will be a mismatch. Customers’ needs should be heard to recommend products that are in their best interests.

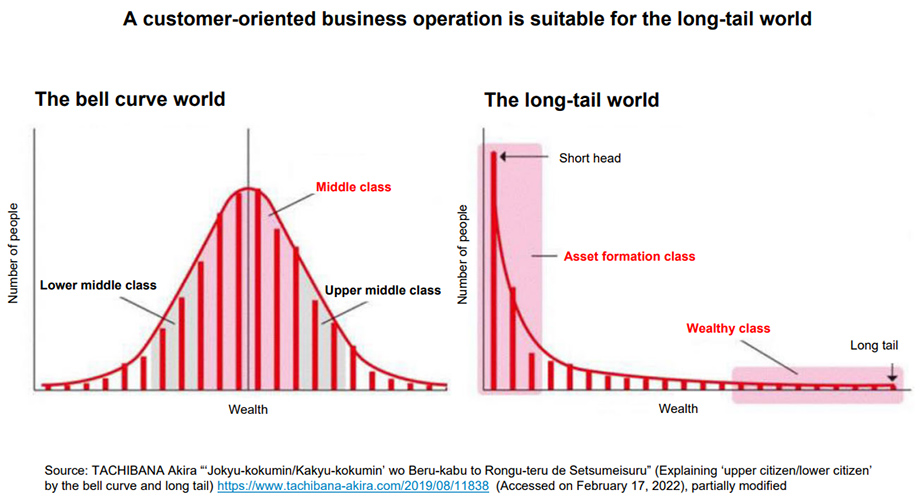

Wealth distribution in Japan and the U.S. used to be bell-shaped, in which the middle-class represented the largest group. Thus, it was just okay to send many sales representatives to mid-to-high asset individuals, and sell financial products with a one-size-fits-all approach. However, at present, it is long-tail shaped, like a dinosaur facing to the left. There is a head to the left side with less assets, and a stretching tail to the right with more assets. There are no volume zones like what we had in the past, and people’s needs and situations are diverse.

In the past, sales representatives were professionals working in the market. But now they need to be professionals for customers and to be customer oriented. If we consider being on track to meet their financial goals as healthy, then they need to carefully listen to the customers’ needs before they sell products. Follow-up after a purchase to see whether the customer is on track is also important. European and the U.S. financial institutions segment customers and focus on their target segments. Japanese firms are also required to understand their customers holistically to support their investment.

Think about your FWB and start investing

In order to wisely engage in investments, it is important to identify your FWB and share your future vision with a professional. When compared to body weight, a BMI (body mass index) can clearly show one’s optimal weight. However, there are personal differences such as “if I try to lose weight to this extent, I don’t feel energetic.” Medical doctors will not just tell people that they need to follow the standard weight but will give advice with their expertise, after considering the personal situation. Conversely, doctors can say what is regarded as best from a large amount of data, but patients need to tell the doctor about their personal condition such as “if so, I do not feel energetic”. Communication is important to reach one’s best state.

After all, you are responsible for your investments. Even if you blindly follow someone’s advice, you are the one who will lose money from a sharp fall of stock prices. Therefore, I hope you will gain financial literacy to the level that you will be able to communicate with professionals and also detect nefarious sales representatives.

So, how can you identify a good financial professional? In the U.S. there is a lot of guidance using three criteria. Firstly: competence as a financial expert. You need to check not only how many years of experience in sales and qualifications, but also whether they are ethical as a professional, such as explaining the commissions and fees properly. Secondly: expertise in attribution of customers. If they give the same advice to a second generation small and medium-sized company owner with inheritance and an executive at a listed company, they may not be customer-oriented. For this, it is a good idea to ask them questions such as “how many customers with a similar profile as mine do you have?” or “if you have a customer like me, what kind of advice would you give?” It is also recommended to have someone with a similar profile (i.e., your co-workers or friends) introduce you to a financial professional. Thirdly: chemistry. However good they are, if you are not motivated, nothing can be done. Traditionally, a good sales representative was a person who led you to a high return, but according to recent research, they are now professionals who make the customer feel engaged. In other words, a financial advisor who makes you feel like you want to be engaged in investment.

In the U.S. they say, “don’t work for money; make money work for you.” It means you should create a mechanism to earn money through investment. You will have a long-standing relationship with your financial advisor, and when some situations such as inheritance come up, your children may also get involved with them. Nevertheless, an American official once sighed that people chose a financial advisor easily without even spending as much time as they do choosing a restaurant.” This is a person to whom you need to disclose your confidential money matters. So, do not expect to find the best advisor easily. Indeed, please look for them with great care and time, as if you are looking for a job or choosing your life partner.

* The information contained herein is current as of October 2023.

* The content of articles on Meiji.net are based on the personal ideas and opinions of the author and do not indicate the official opinion of Meiji University.

* I work to achieve SDGs related to the educational and research themes that I am currently engaged in.

Information noted in the articles and videos, such as positions and affiliations, are current at the time of production.